Focused Insights: The Supercycle Is Under Pressure: Will The "Best of Times" Come to An End? Vol IV, Issue 1

No one has a crystal ball to accurately predict the direction that the U.S. economy, the stock market or the insurance agency and brokerage industry will take in 2025 and beyond.

It feels as if there are good fundamentals in place and the industry has the wind at its back to drive continued growth. Some would suggest that we have ushered in a new presidency that is more pro-business, unseen since the days of President Reagan, while having ushered out the least business-friendly administration on record. Based on some proposed policy changes by the Trump administration, it feels like the country can expect good gross domestic product (GDP) growth and in turn businesses can expect strong earnings growth and sustained margins. Asset values remain very high, having risen to levels unforeseen in the past, and whispers about any chances for recession seems to have faded. It also appears that the term “tax increase” has become a history phrase, for now, perhaps even replaced by “tax reduction.”

While many feel confident with the current economy, there are signs that suggest we could be in for more volatility than what we have experienced over the past few years.

There are still sizable uncertain geopolitical risks and a potential return to inflationary pressure. Could the Trump bump turn into a Trump slump? Whether valid or not, concerns seem to be mounting around the impact on inflation associated with some of President Trump’s proposed and already initiated policies. (i.e., The cost of finishing the Mexican border wall, potential trade wars stemming from U.S. tariffs on foreign imports, and the impact that mass deportation may have on the labor market and wages). This lack of clarity on the future of inflation stems from not knowing whether President Trump is truly foreshadowing his intentions, or simply posturing for a stronger negotiating position. Hence the yo-yo equities market of late.

In any event, an increased inflationary environment could turn the tables from the best of times to something more fragile. If the Federal Reserve (Fed) is forced to tighten monetary policy and increase interest rates to control inflation, it is not impossible to think that the best of times since the great depression could rapidly shift.

The other black cloud that cannot be ignored is that the federal debt as a percentage of GDP is now at 120%, almost doubling from 64% in Q2 of 2008. It cannot be ignored that growth since 2008 has been financed by the unsustainable accumulation of debt and that eventually the chickens are going to come home to roost. The Department of Government Efficiency (DOGE) and the slashing of foreign aid could conceivably put a dent in the federal debt, but at over $36 trillion, it will take more than that.1

The U.S. has been through a prolonged period of economic expansion and wealth creation. It has been so long (15+ years), that it may feel like the new normal. Even if you believe, as we do, that the United States is the greatest nation with the greatest economy AND the insurance industry is the greatest industry in the history of mankind – economic cycles do exist.

It is not realistic to think that we will always be riding on the crest of the wave. At some point our nation will need to make some tough, uncomfortable, painful and even overly aggressive decisions, which, in the short term will impede performance.

But it just might be the antidote to help sustain our economy for long term success. In fact, whether or not you agree with the tactics being pursued by President Trump, we are witnessing some of those tough decisions at this very moment.

Is the insurance industry in utopia or a supercycle?

The insurance agency and brokerage business has been the beneficiary of a great environment. This industry has been blessed by a strong economy, a positive rate environment, strong organic growth and in turn – high profitability. This backdrop has yielded strong capital market support, high firm valuations, record public broker valuations and outstanding returns for private capital investing in this industry. It is such a great environment, many call it “utopia.” However, more realistically, it may actually be a 15-year supercycle.

During the past 15 years, all performance curves seem to only go up and to the right. This industry has seen unprecedented exposure base expansion due to record levels of claims inflation, social inflation and nuclear verdicts. The elongated hard market environment and rising premiums have driven record organic growth, high valuations and seemly unwavering capital market support. 2024 was another year of strong organic growth for the insurance industry, with the average insurance firm achieving organic growth rates reaching 8.7%, and top performing firms (Best 25%) reaching 18.2%.

So, it’s no mystery why the debt market and the equity investment community has been increasingly supporting this industry – given its virtually flawless asset and credit quality.

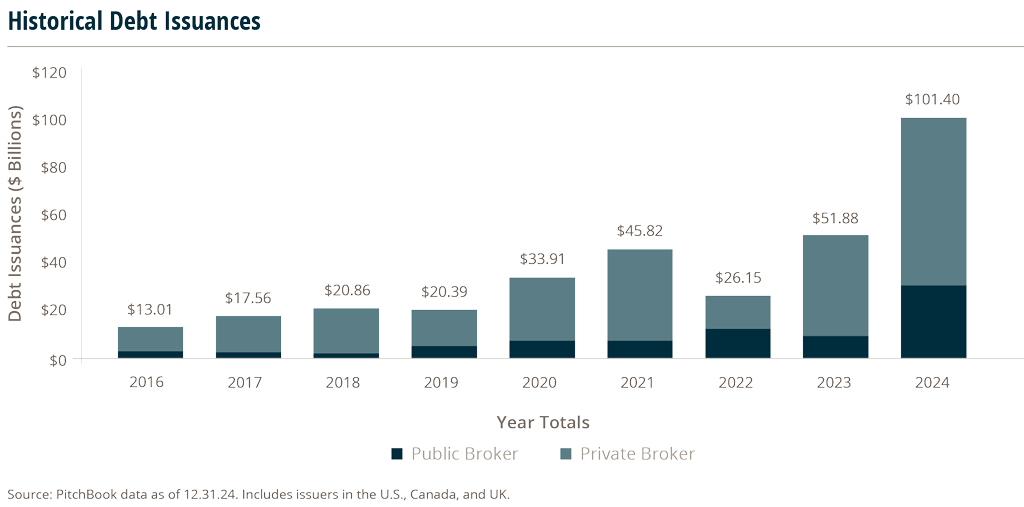

In 2024, there was over $100 billion of institutional rated debt raised in the insurance brokerage industry, the highest amount ever raised in this industry in a single year. If you count unrated private debt, issuances conceivably doubled that.

Private equity-backed brokers with debt equal to 7, 8, 9 and even 10 times EBITDA (earnings before interest, taxes, depreciation and amortization) have almost universally avoided principal and interest technical covenant default let alone principal and interest payment default, which has made the industry seem invincible.

Over the last 15 years, valuations have soared. Public broker valuations, as a multiple of EBITDA, have increased from 9.4x (in 2009) to over 20x (in 2024).

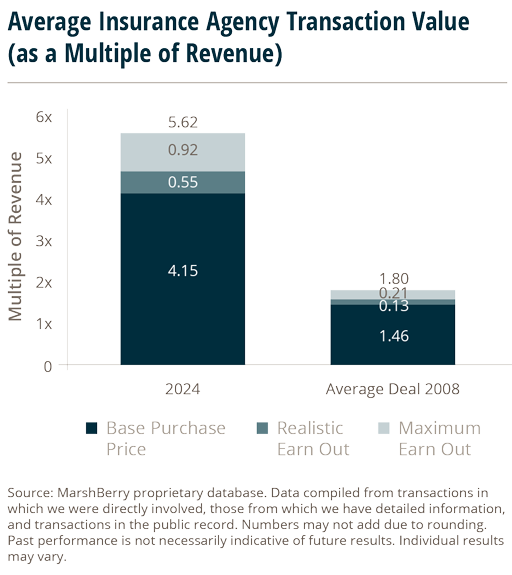

For the average privately held insurance agency, valuations in 2024 increased 315% since 2008 – going from 1.46x to 4.15x as a multiple of revenue at closing. The best firms commanded closing multiples eclipsing 6x revenue during 2024 and the peak was over 9x revenue. And 2008, at that time, 1.46x was a high water mark the industry had yet to experience.

But what if the supercycle comes to an end?

Nobody can predict if, or when, this supercycle will end. But, what if…? What if… the world does not remain at the best place it has ever been. What if… every single graph doesn’t only go up and to the right forever. What if… there is a change in this utopian world and everything isn’t the best that it has ever been? Nobody knows who is swimming naked until the tide goes out.

Valuations have not corrected. But there are signs of potential tightening. The supercycle is under pressure. With the past few years of elevated interest rates, investment returns have been under pressure.

Many are recognizing that some firms’ strong organic growth rates are just a byproduct of external factors, not necessarily due to strong leadership and a robust sales culture. Private equity funded brokers are facing the need to integrate and grow organically to bring in new investors at a valuation on par with internal trading values. Those that can’t or won’t are having trouble supporting the valuations required to satisfy their investors or their internal mark. As a result, some have been and many more may be forced to sell to strategic buyers to get required returns by leveraging cost synergies.

Arthur J. Gallagher (AJG) has publicly said it expects to recognize synergies of approximately $160 million in the AssuredPartners deal over the next three years, adding 10-12% to AJG’s earnings per share.1

It only takes a quick internet search to read that the average privately held insurance agency platform traded for 14.02 times pro forma EBITDA during 2024, which is higher than the trading values of both Assured Partners2 (valuation after subtracting the deferred tax asset) and Woodruff Sawyer3. Some have even called such published marks a “canary in a coalmine.” With the canary making a bird call that seems to foreshadow declining valuations and a wave of private equity backed brokers selling to strategics. Perhaps the call is suggesting that it is not logical for the average $10M revenue insurance agency platform to be worth more than a broker with hundreds of millions, let alone billions, in revenue.

Given that diversification, integration and internal financial controls are now on the radar, there has been a dramatic increase in the forensics of due diligence and a microscope on quality of growth (QoG). It is no longer a question if you are growing – but how you are growing.

Is your growth born of coincidence and externally influenced factors or because you have built a bench and a platform? There is now a growing difference in value between those that are average (growing because of the wind blowing) versus platforms that have infrastructure and are growing by executing organic growth best practices.

What does the future hold for insurance agencies and brokers?

There was a time (in 2012) when base purchase price multiples for insurance agencies and brokers reached a breathtaking 6x EBITDA. That was considered incredible and even unsustainable. Today – some of the worst performing firms in the country can command a double-digit pro forma EBITDA multiple.

Will there be a correction in valuations for insurance agencies and brokers? Will consolidation in this space start to slow down? Will the capital market support begin to wane? Will the most active buyer segment, private equity-backed brokers, be forced to sell to strategics or recapitalize their existing private equity sponsor with a new sponsor at multiples less than they have paid or are paying for the next acquisition?

No one can answer these questions. But keep in mind, despite the record level of debt raised in 2024, a lot of existing dry powder remains undeployed as demand for insurance agencies and brokers continues to outpace supply. Perhaps any increase in inflation or changes in economic conditions in 2025 will have no effect on demand or valuations for quality firms.

However, logical thinking suggests that there has been so much success and such a run up in valuations that we may look back upon today and recognize that we were in the midst of irrational exuberance.

No one knows the future, but some things you can always bet on – the world will not always be the best it has ever been, graphs will not always go up and to the right, and nothing lasts forever.

Sources:

- https://fiscaldata.treasury.gov/americas-finance-guide/national-debt/

- https://investor.ajg.com/news/news-details/2024/Arthur-J.-Gallagher–Co.-Signs-Agreement-to-Acquire-AssuredPartners/default.aspx

- https://investor.ajg.com/news/news-details/2025/Arthur-J.-Gallagher–Co.-Announces-Agreement-to-Acquire-Woodruff-Sawyer/default.aspx